Many early-stage founders in India begin using their personal bank accounts for business payments. At first, this feels simple and convenient. However, as transactions increase, it becomes difficult to track expenses, manage taxes, and maintain financial clarity.

A dedicated business bank account solves this problem early. It helps founders organize finances and create a structured financial system from the beginning.

This guide walks through the key steps founders should follow when opening their first business bank account in India.

Why Your Business Needs a Dedicated Bank Account

Using a personal account for business transactions may work for a short period of time. But as the business grows, it creates confusion and financial complications.

A dedicated business account allows you to:

- Separate personal and business transactions

- Track cash flow more accurately

- Simplify tax and GST compliance

- Build credibility with vendors, lenders, and investors

Opening a business account early creates financial clarity and helps founders manage money more responsibly as the company grows.

Choosing the Right Type of Business Account

Most businesses in India operate through a current account. Banks design current accounts specifically for organizations that handle frequent transactions.

Unlike savings accounts, current accounts support:

- Higher transaction volumes

- Business payments through NEFT, RTGS, IMPS, and UPI

- Cheque issuance

- Business debit cards

- Online banking access

Current accounts are commonly opened by:

- Proprietorships

- Partnerships

- LLPs

- Private Limited Companies

- Registered MSMEs

Choosing the correct account type ensures that daily financial operations remain smooth and efficient.

Documents Required to Open a Business Bank Account

Preparing the required documents in advance helps speed up the account opening process. Most banks require documents from three categories.

Business Registration Documents

- Certificate of Incorporation or Registration

- PAN of the business entity

- GST registration if applicable

- Partnership deed, LLP agreement, or MOA and AOA

Identity Proof of Owners

- PAN cards of directors or partners

- Aadhaar, Passport, or Voter ID

Business Address Proof

- Utility bill

- Rental agreement or ownership proof

- Shop and establishment certificate if applicable

When founders organize these documents beforehand, they reduce delays during verification.

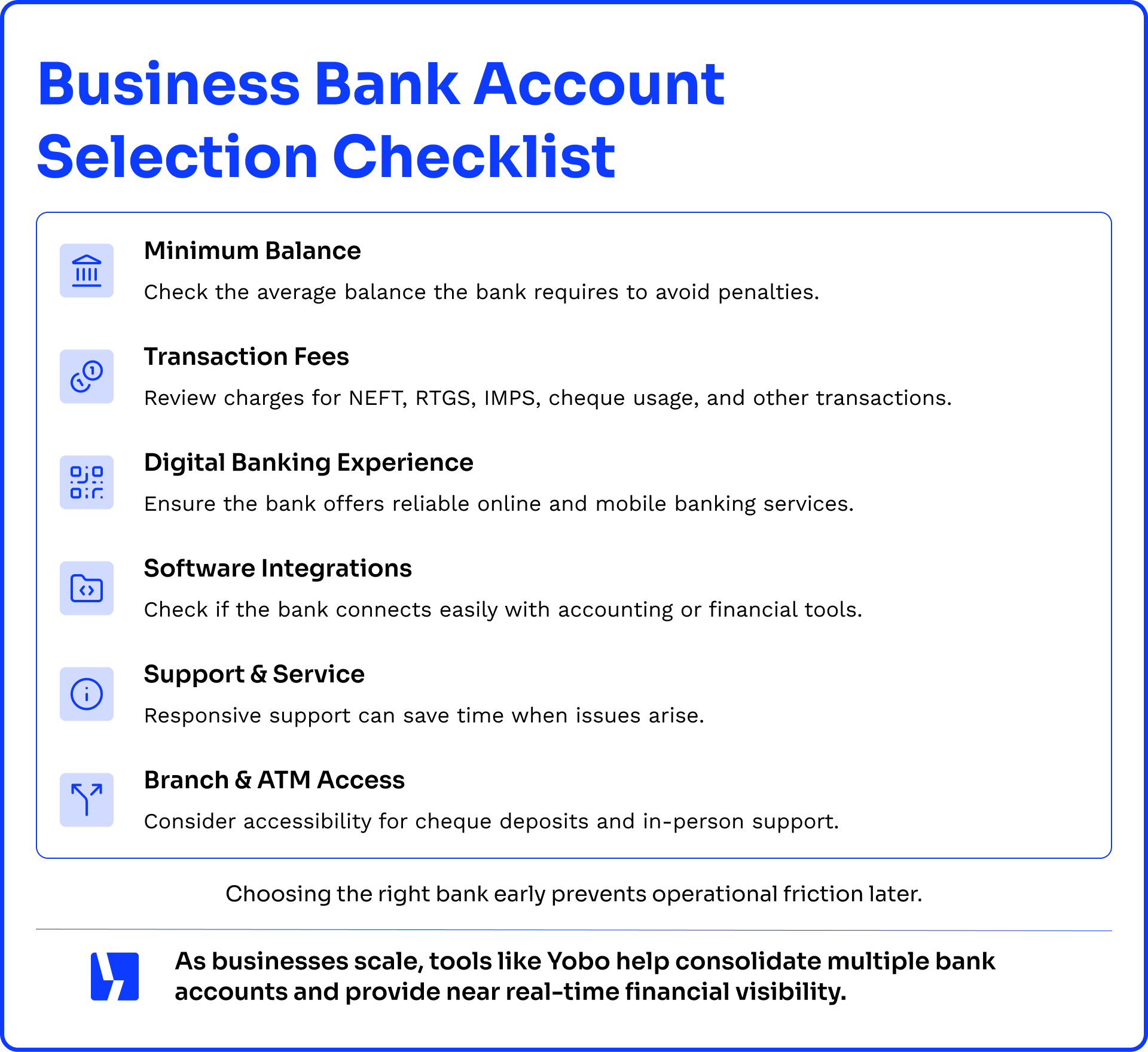

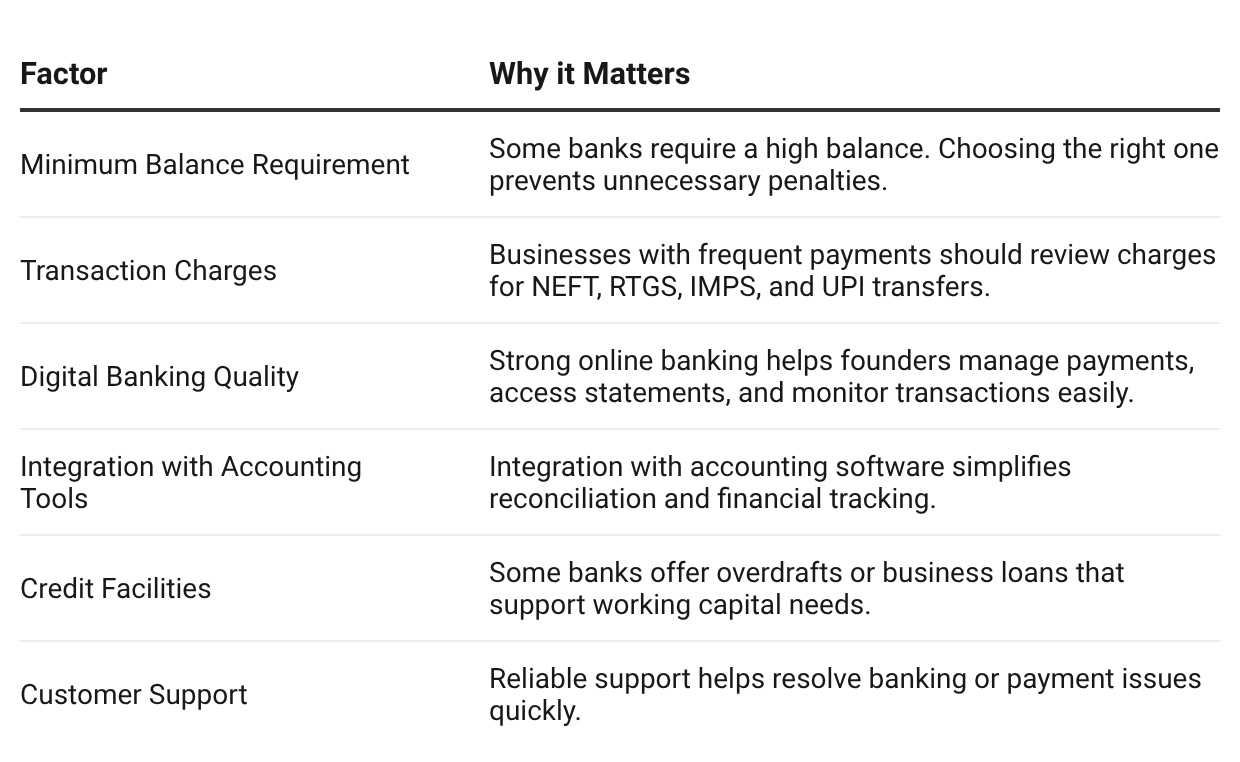

Compare Banks Before Opening an Account

Many founders open accounts at the first bank they approach. However, comparing banks before making a decision can prevent operational difficulties later.

Founders can use the following checklist when evaluating banks.

Choosing a bank that supports both digital banking and operational convenience becomes increasingly important as the business grows.

Completing the Account Setup

Once you select a bank, the account opening process usually involves several simple steps.

These steps include:

- Filling out the bank application form

- Submitting KYC and business documents

- Authorizing signatories for transactions

- Depositing the initial balance

After verification, most banks activate business accounts within two to five working days.

Once the account becomes active, founders should enable digital banking access and configure basic security controls.

Establish Financial Discipline Early

Opening a bank account is the only step. Businesses must also maintain structured financial processes.

Founders should:

- Define clear payment approval roles

- Track inflows and outflows regularly

- Maintain sufficient operating liquidity

- Avoid mixing personal and business transactions

As businesses grow, they often operate across multiple bank accounts for collections, vendor payments, and working capital management. Over time, maintaining visibility across these accounts can become difficult.

Many businesses therefore adopt platforms like Yobo., which help consolidate banking visibility by bringing all bank accounts into a single dashboard, track cash movement, and manage payments and liquidity from a single dashboard.

Common Mistakes to Avoid

First time founders often encounter avoidable problems when setting up their banking structure.

Common mistakes include:

- Using personal accounts for business payments

- Ignoring minimum balance requirements

- Opening accounts without comparing charges

- Allowing unrestricted account access

- Not monitoring cash flows regularly

Avoiding these mistakes early helps businesses maintain financial discipline as they grow.

Final Takeaway

Opening a business bank account is not only a regulatory requirement. It forms the foundation of a company’s financial operations.

Founders who choose the right bank, organize documentation properly, and establish financial discipline early can avoid operational complications later.

As transaction volumes increase, maintaining visibility across accounts becomes increasingly important. With the right financial systems in place, businesses can manage growth with greater clarity and control.