Vendor payments usually start becoming difficult quietly. At first, everything still appears manageable because suppliers are getting paid, invoices are moving, and the finance team is handling requests as they come in. But as the business grows, the process begins to stretch. More vendors get added, payment cycles tighten, and different teams become part of the approval chain. Some payouts are urgent, while others are linked to inventory movement, service milestones, or recurring vendor contracts.

Then familiar uncertainty starts to surface. A team member asks whether a vendor's payment has gone through, but the answer is not available in one place. Someone checks the invoice email, then the finance chat, then the bank portal, and sometimes even after checking multiple places, the status still feels unclear. Nothing has failed, but the process no longer feels fully visible.

This is the point many founders and finance leaders recognise in 2026. The payment workflow still functions, yet it no longer feels dependable enough for the pace of growth.

The Operational Shift Behind Payment Complexity

The real shift is not only about having more transactions. What changes is the way payments behave inside a growing business, where more payments happen at the same time, more people become involved in approvals, and more decisions need to be made every day.

Earlier, payments felt like isolated tasks. A bill came in, someone checked it, and the payment went out. Now, payments are ongoing operations.

They connect procurement, finance, vendor relationships, cash flow timing, and internal accountability. What once felt like an admin activity has now become part of the business's operating rhythm. This is why the pressure feels different. The issue is not simply volume. It is coordination.

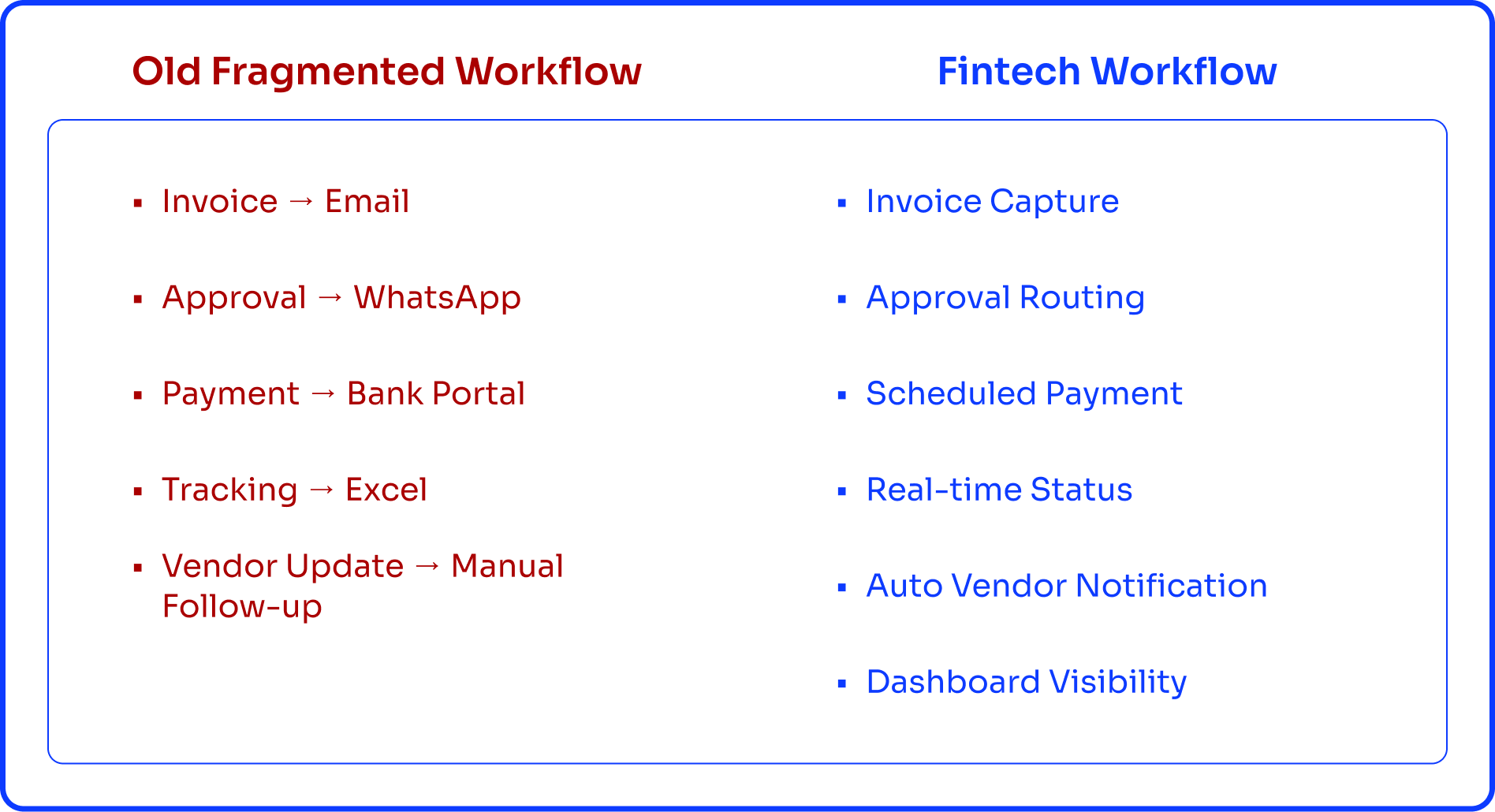

Why Fragmented Workflows Create Payment Friction

The real problem begins when payments no longer happen within one connected flow. The invoice arrives in your email. Approval happens in a WhatsApp message. The payment gets executed through the bank portal. Tracking is updated later in Excel.

Each step works on its own. But together, they do not form a system. Instead of running a structured payment process, the business ends up stitching together separate steps.

This creates small blind spots everywhere. A payment may be approved but not executed. It may be sent but not marked. A vendor may follow up simply because the remittance update never reached them.

The Hidden Operational Cost of Unstructured Payments

The cost rarely shows up as one dramatic failure. Instead, it appears as daily friction.

You double check payments before replying. Your team asks the same status question more than once. Vendors follow up even after the transfer has gone through. Sometimes a payment is delayed simply because one message was missed. Occasionally, the same invoice gets reviewed twice.

None of this feels like a major crisis. That is exactly why it continues. It is not one big failure. It is a small friction repeated daily. Over time, this creates a hidden operational cost. Leadership attention gets pulled into routine clarifications. Finance teams spend more time validating than moving. Vendor confidence weakens because the process feels uncertain, even when payments are technically going out.

How Fintech Is Reshaping Payment Operations in 2026

Fintech innovation is redefining how vendor payments operate.

What was once a series of individual actions is now becoming a streamlined, structured payment flow. Now, payments can be prepared in one place, approvals remain tied to the payment itself, execution follows a clear sequence, and status stays visible throughout the process.

The real difference is visibility. Earlier, the question was, “Did we send the payment?” Now the better question is, “Where is this payment in the process?” That change matters because it removes uncertainty.

Teams no longer need to search across systems to understand status. The flow itself provides the answer. In 2026, this level of operational clarity is becoming the standard expectation rather than an advanced finance capability.

Bringing Vendor Payments Into a Single Operational Flow

This is where platforms like Yobo become useful.

Their value is not simply helping businesses send payments. The real advantage is bringing the entire payment journey into one visible flow. Instead of checking email, chat threads, spreadsheets, and bank portals separately, the process itself becomes easier to understand.

The team knows what is pending, what is approved, what is executed, and what still needs action. That level of clarity reduces follow-ups, improves vendor confidence, and helps the finance function scale without unnecessary complexity.

The Bigger Shift Businesses Need to Make

Vendor payments do not become difficult because a business is growing. They become difficult when the way they are managed does not evolve with that growth. At a certain point, it is no longer about sending money from one account to another.

It becomes about how the business manages approvals, status, visibility, and accountability around every payment. That is exactly how fintech innovations are shaping vendor payments in 2026.

They are replacing scattered actions with structured operational flow. And for growing businesses, that shift means fewer questions, stronger vendor trust, and far better control.

FAQs

Why do vendor payments start feeling difficult as a business grows?

Because more people, approvals, and payment cycles get involved, which makes tracking harder without a clear flow.

How does fintech improve vendor payment visibility?

It keeps approvals, execution, and status updates in one place so teams can see exactly where each payment stands.

Is this useful only for large companies?

No. Even growing startups benefit because it reduces confusion early and builds better financial control.

What is the biggest benefit for founders?

The biggest benefit is fewer follow ups and less need to personally check payment status.